It’s been a whirlwind month since my last post, with the world reeling from tariff hikes and bold policy moves -dare we call them "Trump shocks"? With probably more surprises looming, let’s take the liberty to categorise shocks that the US economy may face into two types: exogenous and endogenous. Understanding these could shed light on the Fed’s expected role in stabilising the economy.

Exogenous Shocks

Exogenous shocks are unforeseen external events beyond the economic system’s control, such as natural disasters, pandemics like COVID-19, or geopolitical crises. These disrupt activity through no fault of domestic policymakers. For instance, COVID-19 triggered supply chain disruptions, business closures, and unemployment surges due to lockdowns, not policy failures. The Fed’s interventions, i.e. lowering interest rates, quantitative easing, or emergency lending, are widely seen as justified to stabilise markets, restore confidence, and prevent deeper recessions. These “bailouts” address temporary disruptions, aiming to bridge the economy to recovery without altering its structure, a role viewed as reactive and neutral.

Endogenous Policymaking Shocks

Endogenous shocks stem from within the economic or political system, often due to flawed or inconsistent policies. “Disorderly” policymaking involves erratic decisions, like contradictory fiscal policies or abrupt regulatory changes, which create uncertainty and destabilise markets. The 1970s stagflation, partly driven by incoherent monetary and fiscal policies, is a historical example. Mitigating such internal failures is complex. While the Fed might stabilise markets through rate adjustments or liquidity, this risks masking poor policymaking and creating moral hazard, where policymakers take risks expecting Fed support. Interventions may be seen as “cleaning up” after policymakers, potentially undermining accountability and delaying reforms.

Key Distinctions and Implications

Exogenous interventions are typically short-term and targeted, like liquidity injections during COVID-19, aiming to restore normalcy without distorting incentives. Endogenous interventions may become recurring, e.g. throughout the next four years, addressing ongoing dysfunction, potentially distorting price signals or inflating asset bubbles. Morally and politically, “exogenous interventions”, like pandemic responses, are less contentious, enjoying strong public support, as seen in bipartisan backing for 2020 stimulus measures. “Endogenous interventions” are more controversial, as they may shield policymakers from consequences, raising fairness and accountability concerns.

Practically, exogenous shocks allow the Fed to focus on immediate stabilisation using tools like rate cuts, suited to temporary disruptions. Endogenous policymaking, often chronic, forces the Fed to navigate political pressures or conflicting objectives (e.g., inflation vs. growth), straining its independence and credibility. Some argue the Fed should intervene regardless, as its dual mandate doesn’t distinguish between shock types. However, this risks overreach, especially for endogenous issues where political or fiscal solutions are more appropriate. While endogenous interventions raise moral hazard concerns, some exogenous bailouts, like 2008 bank rescues, also faced criticism for rewarding risky behaviour.

To sum, exogenous shocks, like COVID-19, are external and temporary, justifying Fed interventions to stabilise the economy. Disorderly endogenous policymaking reflects internal failures, making interventions more controversial and risking systemic flaws. The distinction lies in the shock’s source, the Fed’s role, and the economic and ethical implications. Historical examples and economic theory highlight this divide, though real-world cases often blend both types. Understanding these dynamics helps assess the Fed’s actions and their broader consequences.

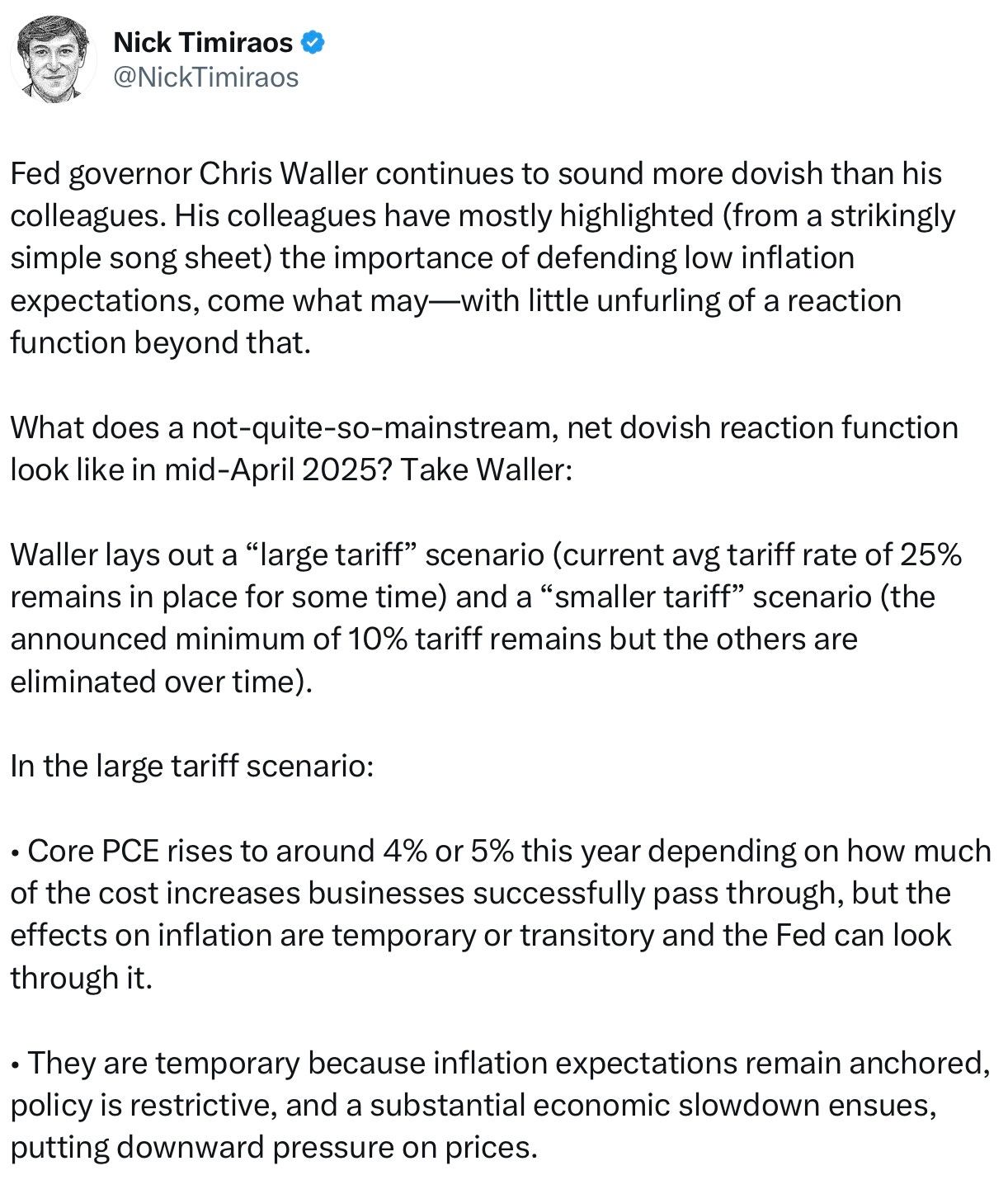

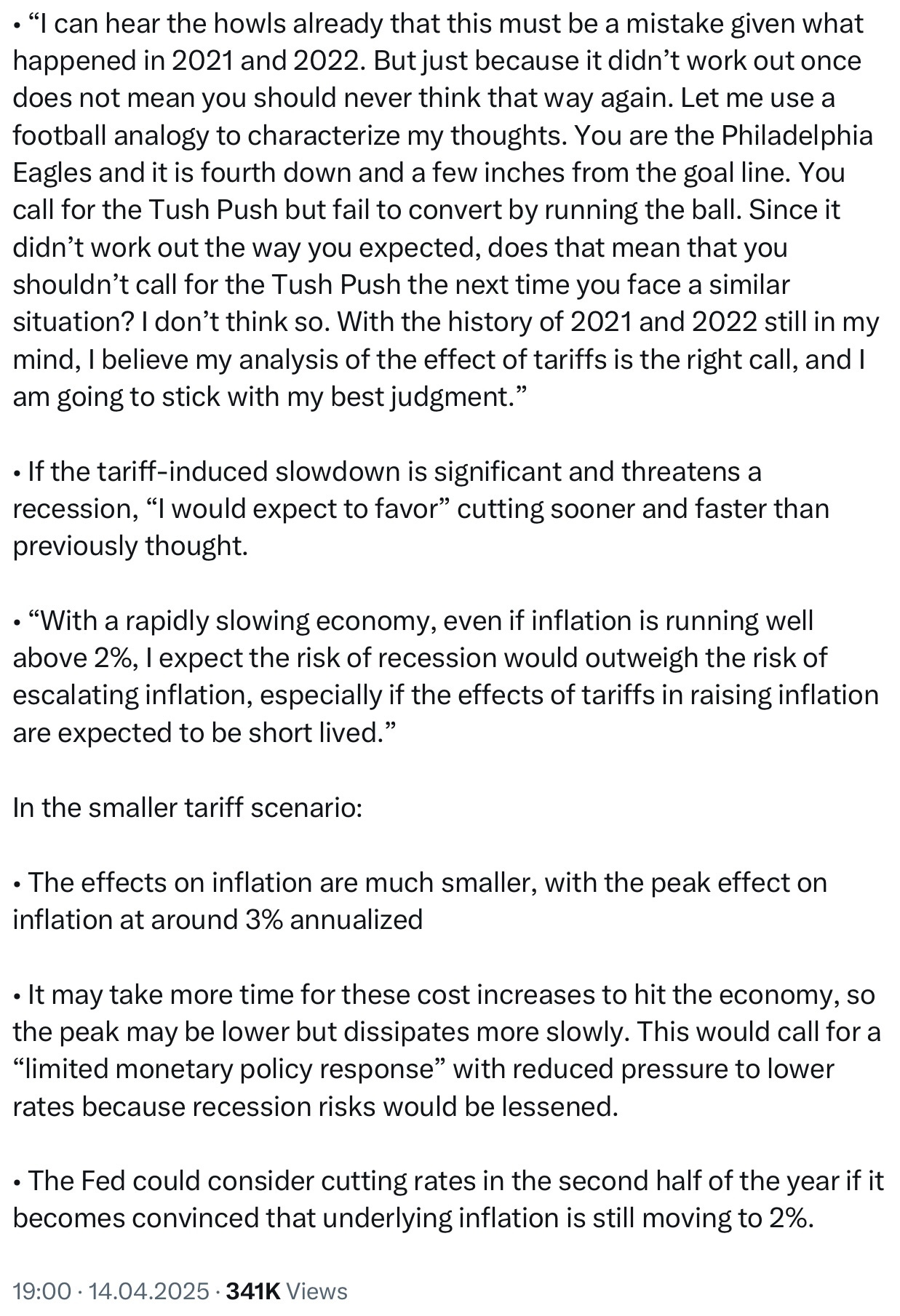

Nick Timiraos, reporting on Waller, tweeted:

Ordinarily, I would agree with Waller, but these are extraordinary times. When a responsible fiscal policymaker is in place, the role of a prudent monetary policymaker is to mitigate economic shocks that threaten price stability and employment to the best of their ability. Thus, Waller's proposal to lower interest rates during economic strain, particularly when a recession looms, despite the threat of inflation, is sound. However, in the presence of an irresponsible fiscal policymaker, who is not only the primary cause of current and impending economic shocks but is also likely to provoke further disruptions during their term, reducing rates could be perceived as the monetary policymaker acquiescing (i.e. monetary policy accommodation) to fiscal recklessness. This risks embedding higher inflation expectations.

Thus far, Trump seems to have a “reaction function” to market movements and probably also to incoming hard data showing the consequences of his policies. Hence, if the Fed mitigates those consequences, it may dampen critical feedback for Trump, potentially encouraging him to continue flawed policies longer. But if the Fed doesn’t, it could enable further economic harm rather than saving it.