Extra credit

How reliable is the credit market as the economy’s “canary in a coal mine”?

The Fed is looking for compelling evidence that inflationary pressures are abating and inflation is heading lower before moderating its hiking efforts. However, validating hiking effectiveness is only half of the diligence that Fed must carry out - hiking itself carries risks to the economy and the Fed needs to monitor these risks as well.

But how does the Fed know when risks have risen to a concerning level? The usual “canary in the coal mine” is to observe how the credit markets behave as credit markets have a significant link to economic activity. In fact, credit is one of the leading indicators should an economy begin to slow down.

Who’s a good canary?

There is a strong and asymmetric relationship between credit spreads and economic growth. The Fed’s FRB/US model indicates that a 100bp increase in credit spreads reduces GDP growth by around 25bp. The level of spreads changes over time in response to changes in financing conditions and the underlying default risk or expected losses. For investors, credit spreads compensate them for macro risks, volatility and liquidity. Thus, credit spreads could give an early indication of economic trouble.

Nonetheless, no leading indicator is without its flaws. Unlike in 2015 and 2018, credit spreads this time may not be as informative as they had been in prior cycles. Market signals may be more muted as balance sheet leverage is continuously declining and companies have high levels of cash. To add, interest rate coverage ratios in credit markets are healthy, most debt maturities are back-loaded, default rates are lower than long-term average and refinancing needs are limited. All these factors make the credit markets less effective as our ‘canary’.

Another reason why we practice caution when using credit spreads as risk indicators is the binary nature of the spreads. Spreads do not spend much time around the mean. Like many markets that vacillate between overreaction of fear and overconfidence of greed, so too do credit spreads. On one side of the spectrum they overshoot sharply when investors fear downturn or fear the Fed is making a policy mistake, while on the other end of the spectrum, they trade very tightly for long periods of time, having too much faith that everything will turn out alright in the end.

Having said that, there is still important information to be had from credit spreads. Widening spreads is an important signal as it can signify a worsening economic environment, although narrowing spreads do not necessarily hail improving economic conditions.

Other than spreads, the vital life-sign of functioning credit markets can be deduced by their liquidity. According to the adverse-selection model of the information sensitivity of debt contracts, when bond value falls, bond liquidity worsens. During crises, there would be large reductions in transactions, both in the primary and secondary markets over a prolonged period of time.

A study entitled “How Credit Cycles across a Financial Crisis” (2017) by Krishnamurthy and Muir demonstrated that a crisis is predated by a huge jump in credit spreads, reflecting a dramatic shift in expectations that surprised markets. The severity of subsequent crisis can be estimated from the change in spreads (expected losses) coupled with the measure of pre-crisis credit growth (financial sector resiliency), and this interplay between expected losses and market resiliency is an important aspect of crises determinant. In addition, the study found that recessions in the aftermath of financial crises are severe and protracted.

The GFC saw the freezing of the structured credit market resulting in a huge fall in the issuance of corporate bonds as well as a sudden decrease in liquidity in secondary markets. Hence, the Fed would take the pulse of credit by keeping tabs on the issuance volumes, or even new issue deals that are being pulled, indicating that issuers are experiencing some jitters. A proviso though, a weak issuance is not necessarily a sign that corporate borrowers are unable to do so, but rather that they have no appetite to issue at, what is to them, extortionately high rates.

A few examples of bonds

Two of the credit spreads we could look at are of investment grade bonds (IG) and high-yield bonds (HY), their all-in yields are currently still in the bottom decile of historical ranges.

Interestingly, US IG have a paradox of having well-behaved yield but poorly-behaved spread. For example, despite the absence of a technical downturn, and based only on a growth scare, IG spreads widened in 2011 and 2016 to a level usually seen during recessions. In contrast, looking further back into history, when the Treasury curve began bear-flattening around 1993 IG spreads decided to do their own thing and kept drifting tighter. As the curve inverted in 1995, IG spreads widened a little but hardly reaching recession levels.

Strange though the behaviour, the market for IG can adjust to higher rates more easily because of yield-oriented buyers, who make up more than half of the sponsorship. However, new regulations on capital can make IG less attractive for some buyers, such as life insurance companies. Front-end yields play an important role in IG credit as IG have become a reliable source for income investors. If front-end yields rise high enough, more investors may be satisfied with risk-free rates and avoid taking on extra credit risk, presenting more competition for IG credit.

The IG market can also be influenced by overseas investors reacting to flattening yield curves. A big portion of IG buyers are made up of Japanese life insurance companies. They own currency hedges via FX swaps that are tied directly to short-term funding rates. Hikes therefore can increase Yen-investors’ hedging costs, making owning US bonds more costly.

As for HY, recession weighs disproportionately on them because in the event of a recession, this asset class is hit by both reduced earnings and greater funding costs. As a result, more of them might go into default. Low net leverage and ample liquidity might help better quality HY issuer, but those of lower quality will find it challenging when faced with higher funding costs. Just over a week ago, USD HY funds saw $6.6 billion of outflows, which is the largest outflow since February 2020 and the fifth largest of all time. Hence, how lower quality credit behaves could be something that the Fed watch out for as an indication of heightened risks.

The mortgage-backed securities (MBS) market came to be as a way to separate mortgage lending from mortgage investing. As a risk thermometer, MBS have a lower beta to broader risk environment as well as lower growth sensitivity compared to IG and others. In the years following Fed’s substantial purchase of MBS in March 2020, spreads on MBS have also tightened sharply.

On the other hand, one thing that has not happened since the mid-1980s but can be observed now, is that the beta of mortgage yields to 10-year Treasury yields has massively overshot to way above one. What this means for mortgage investors is that they would suffer both from higher yields and wider spreads. Three things that may contribute to this are volatile rates market, low liquidity in the secondary market and uncertainty about the path of the policy rate.

This year, as part of quantitative tightening (QT), the Fed has decided to let agency MBS passively run off by not reinvesting matured principal. Considering that the Fed is the single largest agency MBS investor with total holdings of almost $3 trillion as of May 2022, this decision will no doubt affect MBS premiums. This is another thing the Fed would observe, especially if selling off agency MBS from the Fed balance sheet might one day be on the table.

Quantitative tightening and the credit markets

Since we’ve touched on the topic of QT, why don’t we have a closer look at the reaction of credit markets to QT as an indicator. Now that QT is underway, the portfolio rebalancing channel starts working in reverse, widening credit spreads to reflect greater illiquidity premium. As the Fed carries out QT, the source of liquidity stemming from central bank policy will be drained in aggregate from the market. QT affects different assets in different ways. For example, QT impacts rates and therefore MBS through the stock effect, but when liquidity begins to reduce, there will be a direct flow-through for riskier assets such as IG. The effect starts with the widening of MBS spreads and then moves into the corporate credit space.

It’s hard for credit markets to estimate and price the full effects of QT and the associated reduction in liquidity ahead of time. This is because credit is impacted with a lag, i.e. only when the excess liquidity is withdrawn from the markets. Perhaps one way to know is to compare what is happening with historical averages, but this is not that useful either as there has only been one historical QT cycle to analyse.

A further complication in looking at QT effects is that QT this time involves much faster reduction of the balance sheet accompanied by single-minded hiking sessions, as well as slowing economic growth. In other words, effects of QT on credit markets isn’t foreseeable ex-ante.

Stagflation or recession, and default rates

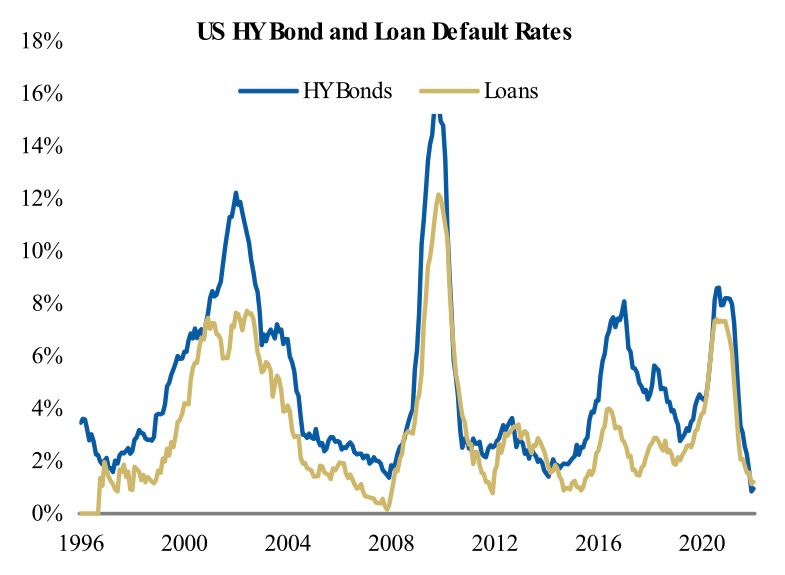

Default happens when a company fails to make timely interest or principal payments and defaults on its bond. Default rate is not a good prediction tool, but it is useful as a ‘nowcast’ tool to see whether we are heading into a recession or not as defaults typically rise during these periods.

The possibility of stagflationary shocks from the Ukraine invasion and slowdown in China makes us wonder, is the risk premium properly compensating investors for these uncertainties? If the geopolitical tensions keep on going and commodity prices remain high, this would obviously affect credit in a major way, even leading to an increase in defaults.

What kind of default rates can we expect should we have a stagflation? To check this out, we can look at whether the EBITDA margins are at a healthy level. EBITDA indicates the cash available for the company to service debt. In the event of stagflation, we might very well see margin compression as cost increases overtake revenue growth.

Note that low margins for companies do not necessarily mean high leverage. Some of them have plenty of cash to withstand any headwinds. In fact, post Covid recession, many companies raised an impressive amount of liquidity that they would probably be ok, cross-fingers barring any further surprises, be they inflationary, geopolitical or otherwise.

Thus far, IG companies seem to feature well in terms of EBITDA margins. High level of EBITDA ensures that the interest coverage ratios (ICRs) are maintained for many more years to come before falling to a more dangerous level. Nonetheless, as financial conditions become tighter and begin to affect corporate earnings, ICRs can turn around sharply to the downside.

Our immediate instinct is to think of hikes as endangering the ability for the companies to service debt, but actually, it is more of what massive hikes can do to expected earnings that is a greater concern. Companies that are already struggling would depend even more on earnings to repair their balance sheets and having big hikes will impair their ability to recover.

The last times stagflation occurred was first between 1973 and 1975 and second in the early 1980s. Even though those periods experienced extreme inflation, much higher default rates were actually observed during the recession in the late 1960s. This might show that the link between high inflation and higher default rates is not as clear cut. If on the other hand, instead of stagflation, we are looking at a shallow recession such as was in the years 1960, 1990 and 2001, we could be looking at a short-lived spike of up to 8-10% in 12-month default rate.

Keep in mind that quality corporate defaults data only started being kept after the mid-1980s. In addition, corporate credit markets have also improved in efficiency and experienced changes in legal requirements. These developments make it more challenging to compare this period’s defaults with previous ones and therefore, whatever default rates projected based on the past are at best, educated guesses.

We should take heart though, that for the past decade default rates have been close to historical lows. Even in the face of a recession, defaults are unlikely to rise significantly considering the quality of corporate credit and corporations having the strongest balance sheets of the past twenty years. There are also a few other reasons why defaults would not materially rise this time, which I may explore in a future post.

A recent Deutsche Bank report disagrees with this, conjecturing that the period of ultra-low default world is ending and that a structural shift upwards in default rates over the years is coming, but this is based on the premise of sustained high inflation throughout the following decade.

Fed as a circuit breaker

Would the Fed actually do something if there are signs of major trouble?

The credit markets look to the Fed to act as a circuit breaker when spreads widen, such that there is an alarming increase in volatility and illiquidity. In the past, there has been a reflexivity between the spreads and the Fed’s reaction function. When credit spreads widened sharply in 2015-2016, 2018-2019 and post Covid, Fed paused its monetary tightening.

Even so, we shouldn’t rely on previous behaviour of the Fed, as this time might really be a whole different kettle of fish. The Fed today does seem to be laser-focused on bringing inflation down such that the Fed might insist on a higher bar before deciding to come to the rescue and temper its hiking.

The path that credit markets are trying to navigate is not an environment of several rate hikes cushioned by a growing economy. Before, the Fed could hike into a healthy economy which means that rates have the luxury of time to adjust in a gradual manner and credit spreads can still tighten far into the hiking cycle.

Now, the Fed is hiking determinedly in the face of high inflation and into a slowing economy with widening credit spreads while the world is still mired in uncertainties. More importantly, it is a situation which has not manifested much in market history. No obvious precedence and therefore, not much past guidance as to what to expect next.

In the longer term, it is the interaction of fundamental factors that anchors credit markets. The robustness of earnings driving balance sheet repair, the level of liquidity buffers providing strength for the companies to endure shocks, the health of the debt service ratios and back-loaded maturities - all these contribute positively to the prospects of fixed income markets and their resiliency to the Fed’s aggressive hiking. In the meantime, the Fed needs to advance cautiously, keeping a watchful eye on the credit canary as it explores deeper into this dark, unchartered coal mine of a hiking cycle.