Oh, the grand old Duke of York

He had ten thousand men

He marched them up to the top of the hill

And he marched them down again

And when they were up, they were up

And when they were down, they were down

And when they were only half-way up

They were neither up nor down

Last year, Powell listed these five justifications why inflation was transitory:

A lack of breadth reflected in trimmed-mean inflation

Moderating inflation in components which have been pandemic sensitive

Wages that remain consistent with inflation goals

Relatively more stable longer-term inflation expectations

Global disinflationary forces.

As we enter the month of May, justifications no. 1 to 3 have been upended, no. 4 is up in the air and as for no. 5, globally, almost everyone is having inflation problems, even the Japanese. For a moment, the FOMC thought they had the luxury to pursue a more equitable aim of ‘maximum employment’ which attempted to be ‘broad and inclusive’. Some have pointed to this ‘activism’ as one of the causes of the high inflation today.

Robert L. Hetzel addressed this “activist policy” in his latest paper, “Learning from the pandemic monetary policy experiment”, saying that by adopting a highly expansionary monetary policy which characterised the 1970s, Powell turned away from prior Volcker-Greenspan policy of raising the funds rate preemptively to preserve price stability. The FOMCs following Volcker-Greenspan rejected an activist monetary policy in favour of neutral policy which concentrated on achieving low trend inflation and unlike Powell, abandoned any attempt to lower unemployment by exploiting the inflation-unemployment tradeoffs* by the Phillips curve.

Whether what the current FOMC tried to do is activism or not, in fairness they could not have known the many shocks the economy was about to encounter - the Ukraine invasion, sky high commodities prices, more China lockdowns - just to name a few. Perhaps the key to pursuing such central bank “activist policy” is to be aware that shocks can come at any time and to perfect the art of pivoting.

Powell himself is not a stranger to pivoting. In 2019, he convinced the board to reverse hiking and helped ease market stress in 2020. Akin to vectors in physics, pivoting is not just a matter of direction, but also quantity.

We could think of the Fed as the conductor of an orchestra and market participants as its members, following the cue of the baton, swinging from slow to fast and to slow again. Of course, the conductor must gain the trust and credibility of the musicians from their many years of performing together. It could then very well be that the better market participants are at following cues, the more freedom the Fed will have to pursue more equitable policies.

Reach For the Stars

The Fed needs to know what the neutral rate is to determine whether the policy is accommodative, neutral or restrictive. When the funds rate is equal to the neutral rate, the policy is said to be ‘neutral’ and when the policy is ‘restrictive’ when the funds rate is above it. The slight hitch with this is that the neutral interest rate is very hard to pin down.

One way to solve this is via the savings-investment framework and estimating the IS curve. The IS curve equilibrates savings and investment in the long-run and shows the effect of the short-term interest rate on the GDP. The Holston-Laubach-Williams (HLW) model can be used to estimate this curve. In their paper, the authors found that the US estimates of the natural rate of interest (the real short-term interest rate that would prevail absent transitory disturbances) have declined dramatically since the start of the GFC and then sat at near zero for many years until 2016.

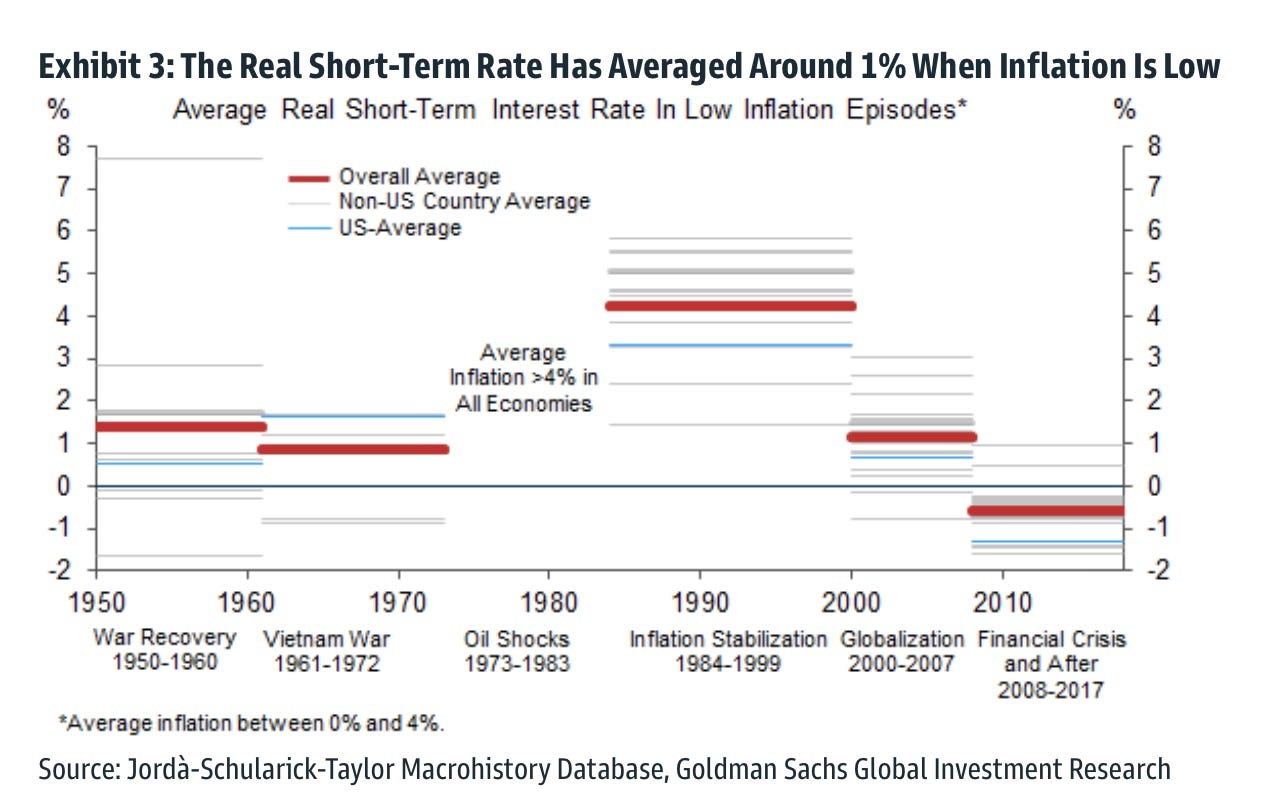

Another way is to look back into history. Oscar Jorda, Moritz Schularick and Alan Taylor in their paper, “Macrofinancial History and the New Business Cycle Facts” (2017) collected the historical database on 17 advanced economies so this database can also be used to make an estimation of r*.

Utilising the database and focusing on the low and stable inflation environments over the postwar period when inflation averaged between 0 and 4%, (which provides the most relevant benchmark for today’s outlook and reduces measurement issues with real rates), Goldman Sachs found that in low and stable inflation environments, r averaged about 1% over the cycle. They also discovered that the post-Volcker 1984-1999 period was an outlier to the high side when policymakers stabilised inflation with very elevated real rates (+4.2%), while the 2008-2017 post GFC period was an outlier to the low side (-0.6%).

Whereas Bullard refuses to provide a long-run dot because he felt that the neutral rate is so indeterminate**, in contrast, Powell peppered his 2018 speech with subtitles bearing the phrase “shifting stars”, such as “Shifting Stars during Normalisation”, “Shifting Stars and the Great Inflation”, “Shifting Stars and the New Economy of the Late 1990s” and the prophetic, “Risk Management in the Face of Shifting Stars”.

Amusing that at the start of his time as chair, he had already an inkling that the neutral rate was going to be an important feature further down the road. Of course, at the time, the main concern was getting off the zero lower bound, rather than managing high inflation. In his 2018 speech, he said, “If expectations were to begin to drift, the reality or expectation of a weak initial response could exacerbate the problem. I am confident that the FOMC would resolutely “do whatever it takes” should inflation expectations drift materially up or down or should crisis again threaten.” The March FOMC projected a 2024 median policy dot at 2.8% above the long-run dot at 2.4%, and this combined with FOMC’s latest favourite word “expeditiously”, show a willingness to move into restrictive territory.

Financial Conditions are Tightening

The IS curve, in essence, shows how monetary policy affects financial conditions and how financial conditions affect the economy.

monetary policy -> financial conditions -> economy

Although the impact of a tightening of financial conditions on the economy is still significant, the sensitivity of financial conditions to monetary policy has weakened massively in the last decades. In the 1960s to the 1980s, there was a strong correlation between higher funds rate and tighter financial conditions. In the 1980s onwards, this relationship broke down. This makes the use of the IS curve and hence, the neutral rate as a gauge of how restrictive monetary policy is on the economy far less useful than it would have otherwise been.

All is not lost however, because we know that even though funds rate alone does not significantly impact financial conditions, the combination of monetary policy innovations and funds rate do. This is not even including other factors that affect financial conditions such as the Ukraine invasion, China lockdowns and other global influences.

Goldman Sachs’ measure of financial conditions, GRI Financial Conditions Index (GSUSFCI) is defined as a weighted average of riskless interest rates, the exchange rate, equity valuations, and credit spreads, with weights that correspond to the direct impact of each variable on GDP.

In 2014/2015, there were around 2.5pts of FCI tightening as the Fed kicked off its hiking cycle in late 2015. In 2018, there were again around 2.5pts of FCI tightening when the Fed hiked every quarter that year. Now, in May 2022, the FCI has tightened by around 1.98pts from the lows. To get a sense of what that means, 1pt move higher in the GSUSFCI is associated with roughly a 1% drag to GDP from financial conditions, 2-3 quarters ahead.

The environment which the Fed faces is very different than 2014/2015 and 2018 periods as inflation today is quite far above the target. Therefore, those previous periods don’t really give us a clue as to how much more of the financial conditions will need to be tightened for inflation pressures to be curbed. In the absence of past examples and foresight of what’s to come, I suppose the best the Fed could do for now is to take it one day at a time.

Estimating the neutral rate goes some way in determining the stance of Fed policy, and monitoring financial conditions gives a sense of the impact of policy on the real economy. With an eye on these as guidance, a self-proclaimed ‘flexible’ Fed will not hesitate to pivot should the situation arise, be it to tame inflation or to mitigate a recession.

———-

*According to some economists, the inflation-unemployment tradeoff is up for debate, which I will not discuss here.

**Bullard and the St Louis Fed believe that forecasting rates should be regime-dependent and therefore, if switches between regimes are not forecastable, the shifts in rates are not forecastable further out either. Looking at the most recent episode of transitory-into-persistent inflation, I’m inclined to believe that they’ve got the right idea.

This is great, I like you writing style. What about the inflation-unemployment tradeoff debate?