The Controversial Phillips Curve

In 1958, W.H. Phillips came up with his famous curve, which shows an inverse relationship between wage inflation and unemployment in the UK (1861-1957). The gist of it was that there is an inverse relationship between inflation and unemployment. Fast forward to today, the modern Phillips curve uses gap variables and expected inflation.

The intuition is that inflation may be driven by the gap between the maximum potential activity of the economy and the actual activity carried out. Formally, the output gap is an economic measure of the difference between the actual output of an economy and its potential output.

Potential output is the maximum amount of goods and services an economy can turn out when it is most efficient (full capacity). A positive output gap occurs when actual output is more than full-capacity output. A negative output gap is the opposite (IMF definition).

Unfortunately, as interesting as this discovery was, the data for the past few decades has not really been supportive of the Phillips curve. In fact, some studies revealed that the correlation between changes in inflation and the output gap has weakened over time.

Measures for A Measure

Even though the Phillips curve today relates inflation to the output gap, we can still proxy that by using the unemployment rate. Is the unemployment rate a good measure for labor slack and hence, suitable to be used for the Phillips curve? Looking at the time varying nature of the labor force participation rate (LFP) and the non-accelerating inflation rate of unemployment (NAIRU), perhaps not. This is because wages react to changes in the output gap with a lag.

Having said that, this doesn’t mean that the unemployment rate is a waste of a measurement when dealing with the Phillips curve. Rather, we could correct for these effects by deflating wage growth either by measuring inflation expectations (through conducting market surveys), or by introducing a one period lag in the part time employment rate as a percentage of the labor force instead of the conventional measure of labor market slack. That way, we do not have to deal with changes in the LFP and estimation of NAIRU over time. Another adjustment could be to try and incorporate changes in the productivity growth.

What Happens When…

What happens when… there is a period of LOW UNEMPLOYMENT? Some research claim that there is convexity in the curve, where inflation begins to accelerate in a nonlinear fashion at sufficiently low levels of the unemployment rate. This is where output is greater than potential, or in other words, where the unemployment rate is significantly below NAIRU. Can you guess what the Phillips curve would look like under this condition?

What happens when… there is a period of HIGH UNEMPLOYMENT? Abundance of labor means that wages and wage growth can fall. However, the fall might not be all the way or even fall smoothly. This is perhaps due to existing minimum wages, or because some workers need to be retained above equilibrium wages for the employers to remain operational. Perhaps someone such as Paul Krugman would phrase this phenomenon as, “downward nominal rigidities in wages”.

It is argued that in an economy with downward nominal wage rigidity, the output gap is negative on average. According to Shekhar Aiyar and Simon Voigts, because it is more difficult to cut wages than to increase them, firms reduce employment more during downturns than they increase employment during expansions; and herein lies the insight: that firms behave differently during downturns and expansions, i.e. they exhibit asymmetric response when adjusting wage costs. Can you picture how the Phillips curve would look like in both situations?

What happens when… after the period of high unemployment, the labor market starts to TIGHTEN AGAIN, for example, just after a crisis? Does the aggregate wage growth seamlessly revert to ‘increasing’? The answer is, not immediately, because the pent-up wage declines from before need to be worked off first. Needless to say, to know the answer to “what happens when” is not as straightforward as some market commentators would have you believe. To note, different cycles can bring out different behaviours in firms and workers. For example, ‘labor hoarding’ as a term has been bandied about recently by some.

Slackety-Slack

Labor market slack exists when there are greater number of workers willing to work a given number of hours than there are available jobs. A lot of slack means there is spare capacity to quickly respond to increase in demand, whereas a full-employment economy will struggle to raise production quickly. Declining labor market slack has made the Fed more sensitive to upside inflation risks and less sensitive to downside growth risk.

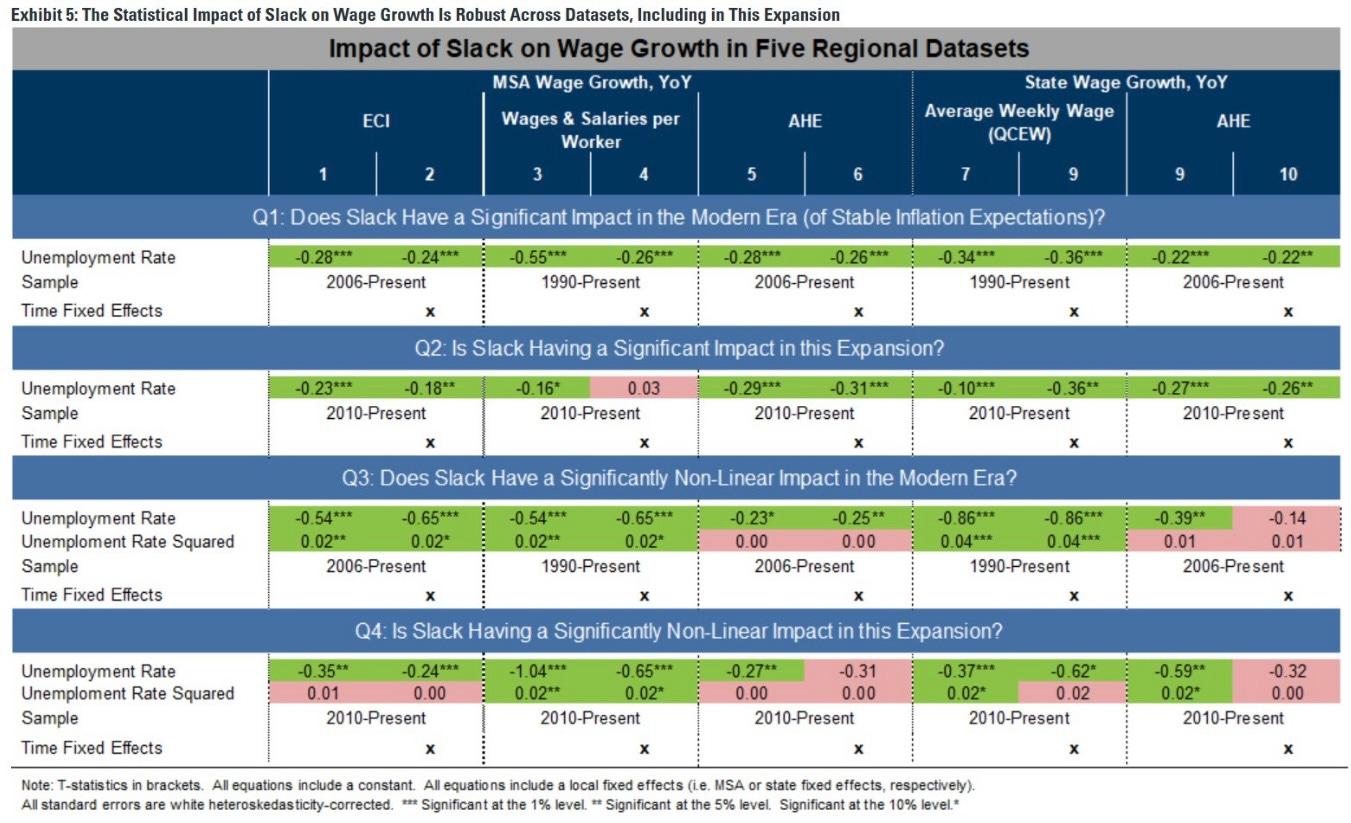

A 2020 Goldman Sachs study finds that declining slack significantly boosts wage growth. The rule of thumb is that a 1.0pp fall in the unemployment rate gap raises wage growth by around 0.3pp. The unemployment rate has a statistically highly significant and very robust effect on wage growth in the modern era of low and stable inflation expectations. The effect of the unemployment rate on wage growth is also statistically significant when looking only at data from the current expansion.

Most datasets suggest that the Phillips curve is non-linear, strengthening at low unemployment rates in the modern era. All this underscore that slack is a key driver of wage growth.

Wage inflation can also be viewed as a function of 1) inflation expectations, 2) productivity growth and 3) the output gap. We’ve already covered the output gap, so let’s take a brief look at the first two:

1) Inflation Expectations

In a 2021 study by Peter Lihn Jorgensen and Kevin J. Lansing, it was shown that in recent decades there is a positive link between the LEVEL of inflation and the output gap, reminiscent of the original 1958 version of the Phillips curve. The study finds too, that gap variables do still exert pressure on inflation despite structural changes in the economy. A reason behind all these may be the improvement of the anchoring of inflation expectations, which makes the inflation expectations component in the Phillips curve more stable. The changing of the behaviour of inflation expectations in response to the evolution of the Fed’s conduct of monetary policy over time, makes for an interesting topic, for another day.

2) Productivity Growth

For over twenty years, real wages have undershot productivity growth, resulting in a falling labor share of income. Corporate profit margins have benefitted from the falling labor share. Faster wage growth means a move towards convergence of real wages and productivity and with it comes increasing labor share of income. Given a set of conditions, corporate pre-tax profit margins should decline in response.

What would corporations do in the face of declining margins? They could raise prices but this is limited as sufficiently high prices can destroy consumer demand. In addition, higher wages may not only reflect slack but also structural shifts. The US is unique among the developed countries in witnessing falling labor share of income since the year 2000. Leading explanation for it is workers’ bargaining power, or rather, the lack thereof. Reductions in unionisation and real minimum wages contributed to this.

However, this trend of falling labor share has reversed since 2015. Labor markets tightened, and alongside it, labor share of income started to increase. The pandemic helped accelerate the reversal. The gap between real wages and productivity began narrowing. Generous pandemic policies amplified the narrowing. For a period of time, the Fed touted “maximum employment” as the overarching goal. America’s ageing demographic trends also point to the tightening of labor markets.

All these show that higher wages relative to productivity growth will remain a feature for some time to come. What does this mean for corporate margins, if, for simplicity, the change in corporate margins is a function of inflation, real productivity and nominal wage growth?

It might mean a fall in pre-tax margins, dependent on the ability of corporations to pass through higher wage costs on to customers. Presumably, larger companies will be able to fare better than smaller companies. Mitigation via technology to replace labor and outsourcing to countries with cheaper labor could be a defence against shrinking margins.

The 1970s created the idea of a dangerous wage-price spiral - higher labor costs leading to increase in consumer prices and in turn, leading to higher wage demands to protect real incomes. Factors enabling this include unionisation and labor contracts that index inflation. But do these still apply today? If companies’ pricing power is limited, rising wages can be absorbed through corporate profit margin compression. As long as this is possible, it can prevent higher labor costs from being passed on to prices.

What Really Happened Post-Everything

For most of the post-war period, the total number of workers has always been above the total number of jobs. In the early 2022, the job-workers gap stood at +2.8pp [i.e. (Job openings in % of labor force) - (Employment in % of labor force)]. This was the highest level it has ever been in the post-war US history. The recent overshoot of jobs relative to workers is a leading candidate to explain the surge in wage growth. Wage inflation around that time was close to 5%, ages after the enhanced unemployment benefits had expired.

One year later in 2023, wage growth has moderated, indicating speedier labor market rebalancing contrary to what is implied by the recent JOLTS job openings report. It seems that the trend in nominal growth has fallen to around 4% (NB: 3.5% wage growth is estimated to be compatible with the Fed’s 2% inflation target).

Digressing a little, what could cause the increase in wages to be more muted than inflation? Firstly, employees would temper wage rise demands if the employees expect the prices of goods and services to rise more slowly in the future. Secondly, if productivity is low, there is a limit to how much bargaining power the workers have. Any further wage demand would eat into the employers’ profit margins. To maintain their profitability, this might force employers to either keep the wages where they are or even fire the workers.

Whereas in Europe, during the pandemic, workers’ support concentrated on preserving existing employment relationships through wage subsidies, the US system abruptly forced temporary layoffs, which may also turn into permanent firings as relationships and ties with former employers weaken over time. This is a highly efficient system if post-Covid the US economy is to go through major structural changes such as large sector reallocations. However, this system becomes a problem if the shape of the economy remains the same as pre-Covid as it introduces further stickiness and major search costs.

In a recent Washington Post article, labor economist William Spriggs says that the US system has allowed service workers previously trapped in low-wage jobs to find better paying jobs in other industries. It seems then, that there has been some small, structural changes in the US economy at least in the lower wage sectors due to the pandemic.

On overall inflation news, for the past three months core PCE inflation has averaged about 3% at an annual rate, closing in to the Fed’s 2%. A part of this disinflation, the word which Powell mentioned 11 times last speech, is because of the recovery of the goods supply chains. Further disinflation can be expected to come from the deceleration in rent and owners’ equivalent rent inflation. So, is it good news all around?

The wise answer is, it’s still to be seen. The labor market poses many questions that still need to be resolved: Are we going to get more surprises in the jobs numbers? How much more room does the labor supply have for it to recover? Will wage growth continue to slow down? What’s the reaction function of the Fed to all these mentioned?

LFP rate has returned to the trend before the pandemic and the labor supply shortage seems to instead come from a reduction in average work hours. The job-workers gap has shrunk to about 4 million in January (averaging the job openings reported from LinkUp and Indeed). This is 2 million above the numbers before the pandemic and is a result of the decline in job openings rather than any painful increase in the unemployment rate. It is the largest decline in job openings outside a recession in US history without any increase in the unemployment rate. Layoffs in the tech sector though, are not representative of what’s going on elsewhere, especially at the lower-wage end.

It seems that the Fed still has some work ahead in reducing the size of the job-workers gap. The Fed’s hiking seems to be shrinking many things inflationary but moving forward, the major focus will be on the Fed being able to cool down the service sector and bring wage growth down to a rate that supports its inflation target.

What Powell and the Fed don´t get is that a flat Phillips Curve is not an assumption but the outcome of a High Quality MP. They have important choices to make, but the answers will not come from studying the problem from a unemployment/inflation perspective, but from, as I argued here, an NGDP Level & growth perspective.

https://marcusnunes.substack.com/p/kernels-of-truth